NRI Inheritance of Indian Property - What Happens After the Owner's Death?

- CA Bhavesh Panpaliya

- May 20

- 5 min read

"My father passed away last month. He owned a flat in Pune and a small piece of land in our village. I live in Canada. What do I do now?"

This is one of the most emotionally difficult questions that lands in a CA's inbox. And honestly, it's also one of the most legally layered. For an NRI inheriting Indian property, the process touches at least three different legal frameworks at once - the Indian Succession Act, the Foreign Exchange Management Act (FEMA), and the Income Tax Act. Navigating all three while grieving, from thousands of kilometres away, is genuinely hard.

This guide walks you through exactly what happens - step by step - when an NRI inherits property in India. No jargon overload. Just practical clarity.

Can an NRI Legally Inherit Property in India?

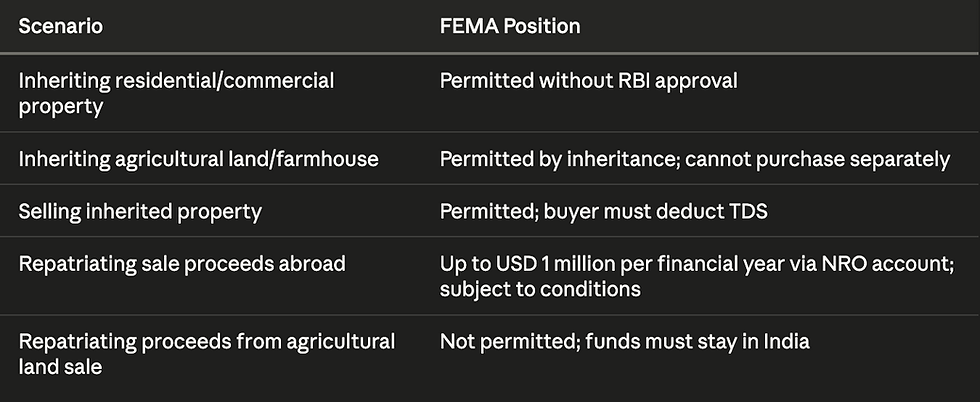

Yes. An NRI can inherit any type of immovable property in India - residential, commercial, or agricultural - from a person resident in India. This is explicitly permitted under FEMA regulations and the provisions governing NRI property rights.

The legal basis for inheritance in India is typically governed by either the Indian Succession Act, 1925 (for non-Hindu individuals or where a Will exists), or personal laws like the Hindu Succession Act, 1956 for Hindu, Sikh, Jain, and Buddhist families.

Step One: Establish Legal Ownership

Before any tax or FEMA question arises, you need to legally establish that the property now belongs to you. Depending on whether the deceased had a registered Will or not, this works differently.

When There Is a Registered Will

Obtain Probate of the Will from the competent civil court (mandatory in cities like Mumbai, Chennai, Kolkata)

In states where probate is not mandatory, a registered Will along with a death certificate may be sufficient for mutation

Get the property mutated in your name at the local municipal or revenue authority.

When There Is No Will (Intestate Succession)

Apply for a Legal Heir Certificate or Succession Certificate from the civil court

All surviving legal heirs must typically be parties to or consent to the process

Once the certificate is obtained, mutation of the property can proceed

These steps are India-side legal formalities and do not yet involve FEMA or income tax. But they are the foundation — without a clear title, nothing else can move forward.

Step Two: Understand the FEMA Position

This is where NRI inheritance becomes different from a resident Indian's inheritance. The Reserve Bank of India (RBI) and FEMA regulations govern what an NRI can do with inherited property and proceeds.

The good news: inheriting property itself requires no RBI approval. The complications arise when you want to sell it or repatriate (transfer abroad) the sale proceeds.

The USD 1 million repatriation limit per financial year is a critical cap. If the property value exceeds this, the funds can sit in your NRO account but moving them abroad requires either waiting across financial years or seeking specific advice on your options.

Step Three: Income Tax on Inherited Property

Here is something that surprises many NRIs: inheritance itself is not taxable in India. There is no estate duty or inheritance tax currently in force. So receiving the property does not trigger any tax event.

Tax comes into the picture in two specific situations:

1. Rental Income from the Inherited Property

If the property is rented out after inheritance, the rental income is taxable in India for the NRI. Tax is deducted at source at 30% under Section 195 of the Income Tax Act. The NRI must file an Income Tax Return in India declaring this income and can claim applicable deductions.

2. Capital Gains on Sale of Inherited Property

When the NRI decides to sell, capital gains tax applies. The holding period is computed from when the original owner acquired the property — not from the date of inheritance. This often means the property qualifies as a long-term capital asset, taxed at 12.5% without indexation benefit (as per the Finance Act 2024 amendments effective from FY 2024-25).

Step Four: After the Sale, Repatriation Process

Once the sale is complete and TDS has been deducted, the net proceeds go into the NRI's NRO (Non-Resident Ordinary) account in India. From there, to transfer funds abroad:

Obtain a CA certificate in Form 15CB certifying the nature and source of funds

File Form 15CA online on the Income Tax Department portal

Submit both to your bank along with the required documentation

The bank processes the remittance within the USD 1 million annual limit

This process is manageable but documentation-heavy. Banks are strict about compliance, and any mismatch in documentation causes delays. Getting a CA to handle Form 15CB is not just a legal requirement - it is practically essential.

Common Situations That Complicate NRI Inheritance

Multiple heirs - If siblings in India and abroad are co-heirs, a family settlement deed or release deed may be needed before a clean title can be established

Property in a rural area - Mutation processes vary significantly state by state; some require physical presence or a power of attorney

Disputed properties - Legal proceedings in India require either physical presence or a registered Power of Attorney (PoA) in favour of a trusted person in India

Property with an outstanding loan - The inherited property may carry an existing mortgage; this needs to be addressed before any sale

Frequently Asked Questions

Does an NRI need RBI approval to inherit property in India?

No. An NRI can inherit any immovable property in India - including agricultural land - without requiring any approval from the RBI or any government authority. The complications arise only when selling the property and repatriating funds.

Is inheritance taxable for an NRI in India?

No. Receiving inherited property is not a taxable event in India. There is no estate duty or inheritance tax. Tax arises only when the inherited property generates rental income or is eventually sold, triggering capital gains.

Can an NRI sell agricultural land inherited in India?

Yes, an NRI can sell inherited agricultural land to an Indian resident. However, the sale proceeds cannot be repatriated abroad - they must remain in the NRI's NRO account in India. This is a FEMA restriction specific to agricultural land.

What TDS rate applies when an NRI sells inherited property?

The buyer must deduct TDS at 12.5% on the entire sale consideration (for long-term capital gains) under Section 195. The NRI can apply for a lower TDS certificate under Section 197 from the Income Tax Department, which can reduce this deduction significantly based on the actual gain.

How much money can an NRI repatriate from inherited property sale in India?

Up to USD 1 million per financial year can be repatriated from the NRO account. This requires a CA certificate in Form 15CB and filing of Form 15CA. If the sale proceeds exceed this limit, the balance can be transferred across multiple financial years.

Does an NRI need to be physically present in India to manage inherited property?

Not necessarily. An NRI can execute a registered Power of Attorney (PoA) in favour of a family member or trusted person in India to handle mutation, sale, and related legal formalities on their behalf. However, some legal proceedings may require personal appearance.

Comments